Now hiring!

Price manipulation is one of the most reliable ways to drain a DeFi protocol. In 2024 it ranked as the second most damaging attack vector in DeFi, accounting for around $52 million across 37 separate incidents, much of it extracted in single atomic transactions that were over before anyone could react.

This overview categorizes the common vulnerabilities and sets out remediation strategies for developers and security auditors.

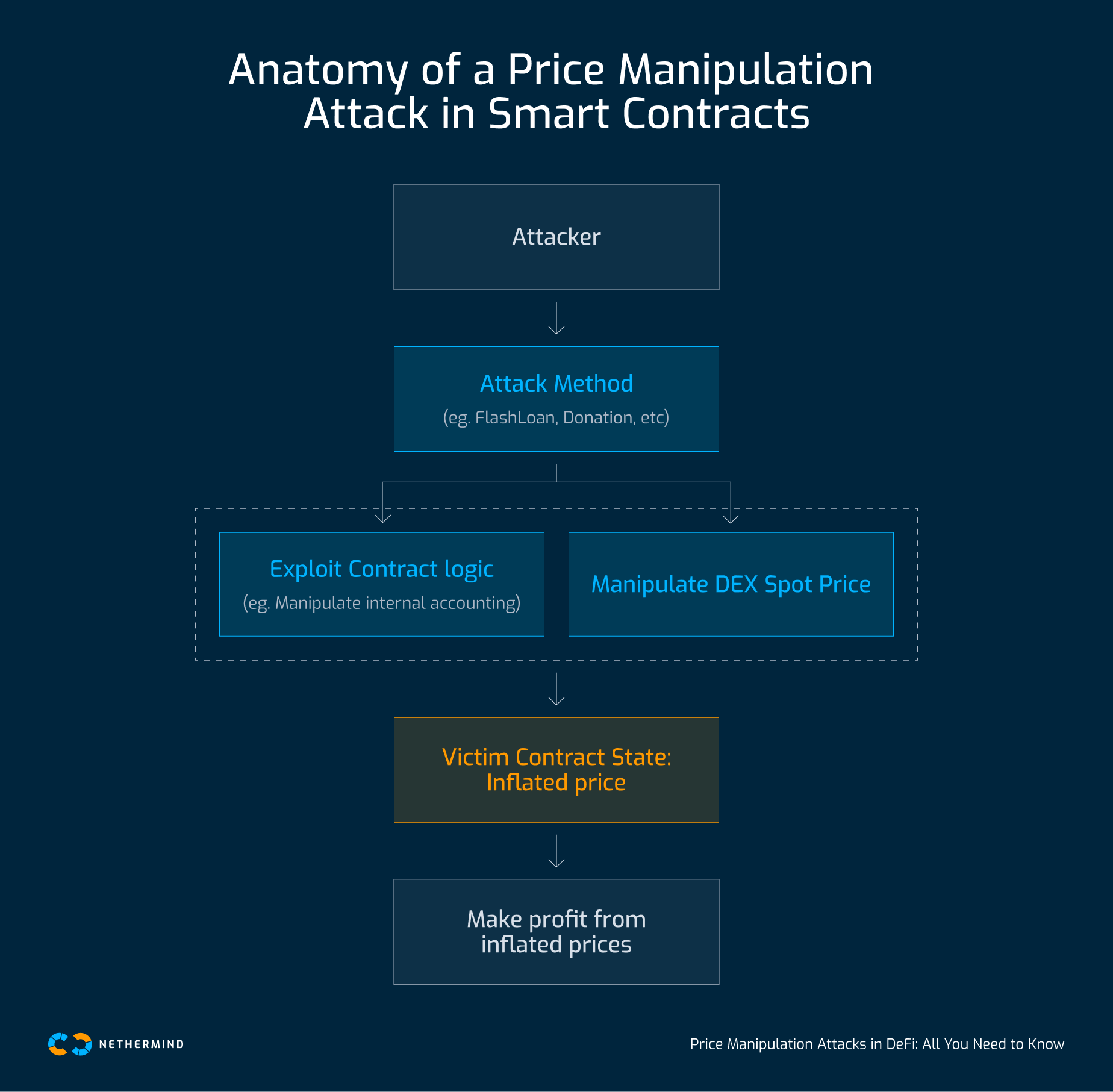

In simple terms, a price manipulation attack involves artificially inflating or deflating an asset's value to profit from the resulting misvaluation. To run these attacks at scale, attackers frequently use flash loans, which let them borrow large amounts of capital with no collateral, provided the loan is repaid within the same atomic transaction. By injecting that liquidity into a DEX pool, or by exploiting a vulnerable contract or oracle, the attacker creates a temporary price discrepancy and then extracts value from it.

Understanding price manipulation begins with how smart contracts calculate prices. Three approaches are common:

Some protocols determine asset value from internal state, such as the ratio of two tokens held within the contract. This approach is highly vulnerable to donation attacks and flash loan manipulation, because an attacker can alter balances through flash loans or direct donations and cause wild price swings.

Consider a vault that sets its share price by dividing total assets by the total supply of shares:

An attacker can donate a large amount of Token A directly to the contract address, using a plain transfer rather than the protocol's deposit function. If the logic relies on balanceOf(address(this)), the share price inflates instantly, with no actual trade taking place. This pattern shows up as a vault inflation attack on new protocols with low liquidity.

Best practice: use internal trackers (state variables) for contract balances rather than relying on the balanceOf() function. Alternatively, ensure the contract state cannot be manipulated through direct transfers.

Because the formula above estimates price from supply and demand within a single contract, an attacker can also use a flash loan to move the price sharply within one transaction. By temporarily draining one side of the ratio, they force the contract to calculate a distorted price and exploit it before the transaction ends.

Another approach queries spot prices directly from DEXs such as Uniswap, SushiSwap, or PancakeSwap, usually by reading current reserves.

Uniswap v3 slot0

In Uniswap v3, the slot0 variable holds the sqrtPriceX96, which reflects the most recent trade. It is accurate for that exact moment but extremely manipulable within a single block. A typical sequence is:

slot0 price.

Uniswap explicitly advises against using slot0 as a direct price source because of this short-term manipulability. It recommends its onchain oracle library instead, which gives a more reliable method for obtaining price data. See the Uniswap oracle documentation.

The Polter Finance exploit in November 2024 shows the cost of ignoring that advice. The protocol priced its newly listed BOO market directly from SpookySwap's liquidity pools, so an attacker used a flash loan to drain BOO from the pool and inflate its quoted price. With the reserves skewed, the protocol's oracle valued a single BOO token at roughly $1.37 trillion.

The attacker posted a token as collateral, borrowed against that fictional value, and left with about $12 million.

To reduce the volatility of spot prices, many protocols use a time-weighted average price (TWAP). Rather than a single snapshot, a TWAP averages an asset's price over a set duration, for example 30 minutes or one hour.

Manipulating a 30-minute TWAP would require an attacker to hold a distorted price on a DEX across many blocks. That makes the attack both cost-prohibitive and high-risk: arbitrageurs would trade against the artificial price and erode the attacker's position, and holding a lopsided position for 30 minutes exposes them to ordinary market volatility. TWAP is not perfect, though. During sharp market moves, a TWAP can lag the real price and produce stale data that remains exploitable.

External price oracles act as a bridge, giving smart contracts access to offchain pricing information. By querying an oracle, a protocol can establish an asset's current market value without depending on its own internal liquidity.

Oracles do not remove risk, though. They shift it from the contract's internal logic to the oracle's data integrity. Common weaknesses include:

Note: oracle-related price manipulation is a large topic in its own right. The examples above illustrate common risk factors rather than a complete taxonomy. For deeper analysis, study real-world oracle exploits.

Chainlink price feeds are a widely adopted oracle solution that uses a decentralized network of nodes to fetch and validate data. When a protocol relies on a Chainlink feed, several practices apply:

updatedAt timestamp against the current block.timestamp. If the elapsed time exceeds your chosen threshold, treat the data as stale. Set that threshold to suit your use case.

Securing a DeFi protocol against price manipulation calls for a layered approach. Internal balances are simple to code and simple to exploit. Decentralized oracles, well-designed TWAPs, and automated circuit breakers each reduce exposure, but none is sufficient alone. The protocols that survive treat price as something to be defended in depth, not read once and trusted.

The Leading Engineers of Blockchain Infrastructure

Nethermind © 2026

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)